Why Buying Beats Renting in San Diego: The Wealth Gap Every First-Time Buyer Needs to Know

🏡 Why Buying Beats Renting in San Diego: The Wealth Gap Every First-Time Buyer Needs to Know

San Diego is one of the most desirable places in the world to live—sun, surf, strong job market, unbeatable quality of life. But if you're renting here (especially long-term), you’ve probably felt the sting of rising rent, limited control, and the feeling of paying someone else’s mortgage.

Meanwhile, homeowners in San Diego are quietly building wealth in the background—sometimes without even realizing it.

And according to the National Association of Realtors, the difference is staggering:

-

Average net worth of a renter: $10,000

-

Average net worth of a homeowner: $430,000

(That’s 43 times higher.)

This massive wealth gap isn’t an accident—it’s the result of one simple truth:

Homeownership builds long-term financial stability in a way renting never can.

If you’re a first-time buyer, a renter considering ownership, or a military family PCSing to San Diego, this guide will show you exactly why buying is the smartest long-term move—and how to do it even in a competitive market.

🌴 Chapter 1: San Diego Reality Check — Renting Costs You More Than You Think

Let’s be honest—San Diego rent isn’t cheap.

Most renters feel the squeeze each year when renewal notices arrive with a nice little bump in price.

But the real cost of renting isn’t the monthly check.

It’s the missed opportunity.

When you rent in San Diego, you’re:

-

Paying someone else’s mortgage

-

Funding someone else’s retirement

-

Missing out on equity growth

-

Giving up tax advantages

-

Losing the stability of fixed housing costs

Meanwhile, your landlord enjoys:

-

Equity gains

-

Appreciation

-

Tax write-offs

-

Consistent cash flow

-

Growing net worth

You are literally contributing to someone else’s $430,000 in wealth.

And San Diego, with its historically strong appreciation, makes that wealth grow even faster.

🏆 Chapter 2: Why Homeownership Creates Wealth (Even When Prices Feel High)

You might be thinking:

“How does buying make sense in this market? Prices are high.”

You’re right—San Diego isn’t the cheapest city.

But high prices don’t prevent wealth building; they accelerate it.

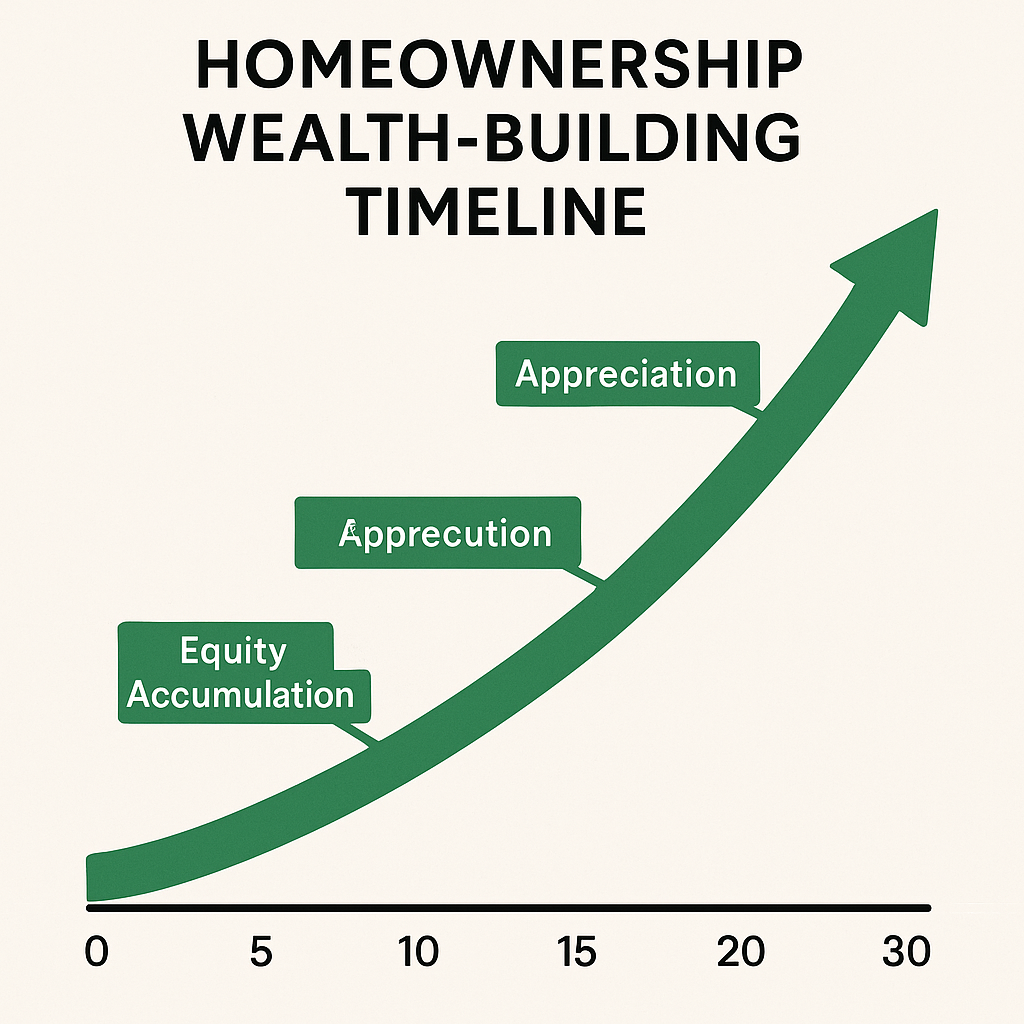

Here's why homeowners build wealth automatically:

1. Appreciation (San Diego averages 5–7% annually)

Historically, San Diego homes appreciate faster than most U.S. cities.

2. Equity accumulation

Your loan balance goes down month by month.

3. Fixed housing cost stability

Rent rises; mortgages stay stable.

4. Tax benefits

Mortgage interest deduction

Property tax deduction

Capital gains exclusion

5. Forced savings

A home is a built-in wealth savings account.

These benefits compound over time—and that’s why the average homeowner ends up with nearly half a million in net worth.

🎖️ Chapter 3: A Special Advantage for Military Buyers PCSing to San Diego

Military families PCSing to San Diego have a secret weapon:

The VA Loan.

And it might be the best loan product in the country.

Why military buyers LOVE the VA loan:

-

$0 down payment

-

No PMI ever (huge savings)

-

Flexible credit requirements

-

Competitive interest rates

-

You can reuse it (yes, really!)

-

You can buy again after PCS sales

Many service members use the VA loan to begin or expand a real estate portfolio.

Real Example (completely typical):

A Navy client of mine bought a townhome in Clairemont, lived in it 3 years, then PCSed.

Instead of selling, they kept it as a rental.

Today:

-

Mortgage: $2,100/month

-

Rent: $3,200/month

-

Appreciation over 5 years: over $210,000 in equity

They now have a cash-flowing asset that someone else is paying off.

This is how military families go from renters to generational wealth holders.

🏘️ Chapter 4: “But San Diego Is Too Expensive…” (Let’s Bust That Myth)

Here’s the truth:

Homes ARE expensive…

but so is renting.

And thanks to modern lending options, first-time buyers have more paths to homeownership than ever.

You may qualify for:

➡️ VA Loans (0% down)

➡️ FHA Loans (3.5% down)

➡️ Conventional 3% Down First-Time Buyer Loan

➡️ Down Payment Assistance Programs (CalHFA, MCC, city grants)

➡️ Seller Credits to cover closing costs

➡️ Rate Buydowns negotiated by your agent

➡️ Discounted homes from motivated sellers

Many renters don’t realize that they could buy right now with less than ONE month's rent as their down payment.

🏷️ Chapter 5: How to Find Deals in San Diego (Yes, Real Deals Exist!)

Even in a competitive city like San Diego, there are always:

-

Overpriced homes sitting on market

-

Homes needing cosmetic updates

-

Sellers relocating

-

Military sellers PCSing under deadlines

-

Investors offloading rentals

-

Divorce, job changes, probate situations

-

Price-reduced listings

-

Homes with “reverse offers” (yes—sellers offering incentives)

The key is working with an agent who knows where to find them.

Here’s how I uncover the best opportunities for my clients:

✔️ Daily MLS data sweep

Identifying price reductions & stale listings.

✔️ Private agent-to-agent networks

Where deals are often shared before hitting the MLS.

✔️ Off-market and coming-soon lists

Great for military buyers arriving before house-hunting leave.

✔️ Identifying motivated sellers

Notice of relocation, job changes, or vacant homes.

✔️ Negotiation strategy

Rate buydowns, closing costs credits, and purchase price reductions.

With the right guidance, deals aren’t only possible—they’re common.

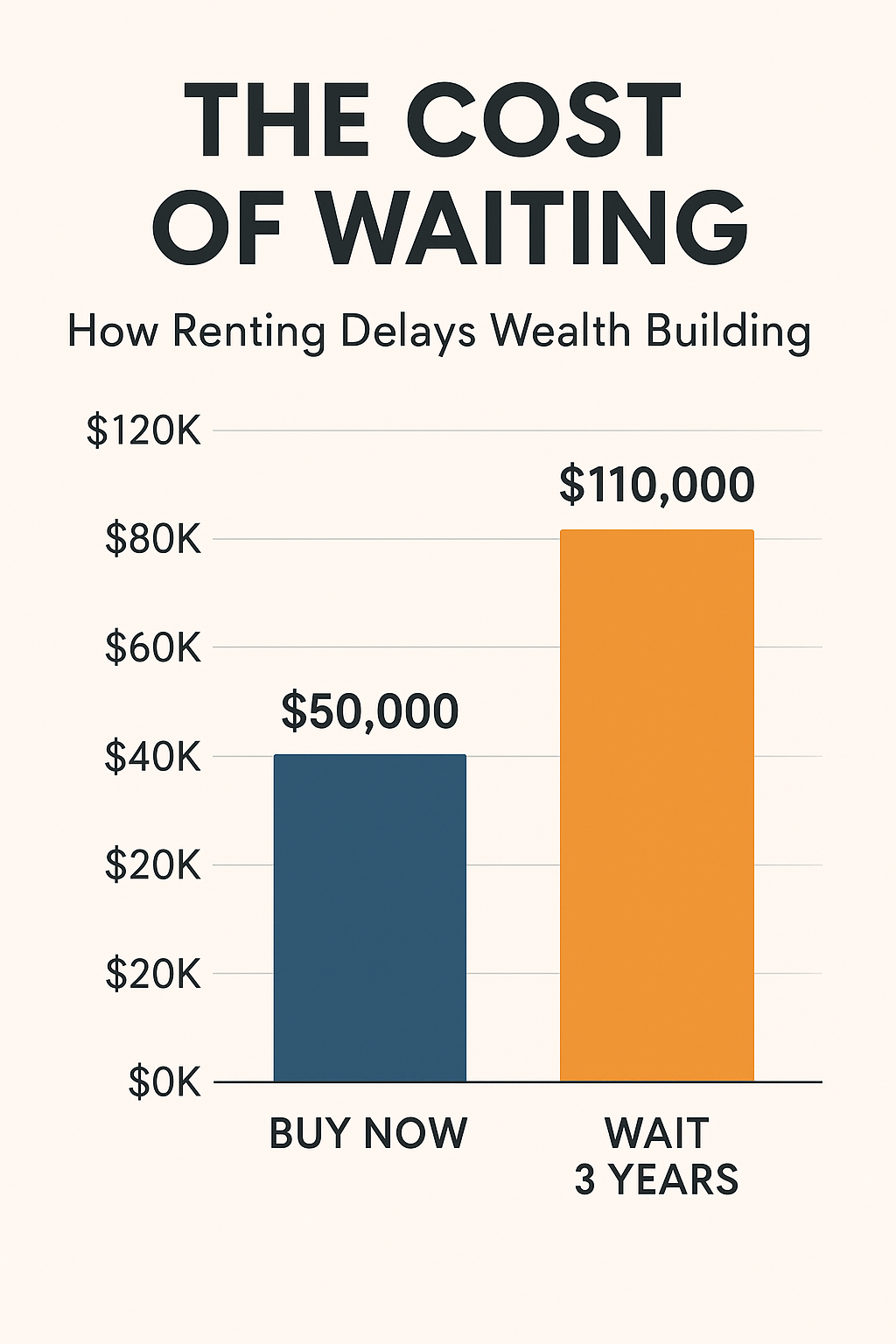

💸 Chapter 6: The Hidden Cost of Waiting

If you’re renting now and planning to “wait until next year,” here’s the truth:

You’ll likely pay more.

Historically in San Diego:

-

Home prices trend upward

-

Rent trends upward

-

Mortgage rates fluctuate unpredictably

Even a 1% change in interest rate can cost (or save) you hundreds per month.

Example:

A $700,000 home at 5% vs 6% is a difference of $400+ per month.

Meanwhile, home values may increase another 5–7%.

Waiting is not neutral.

Waiting has a cost. A very real one.

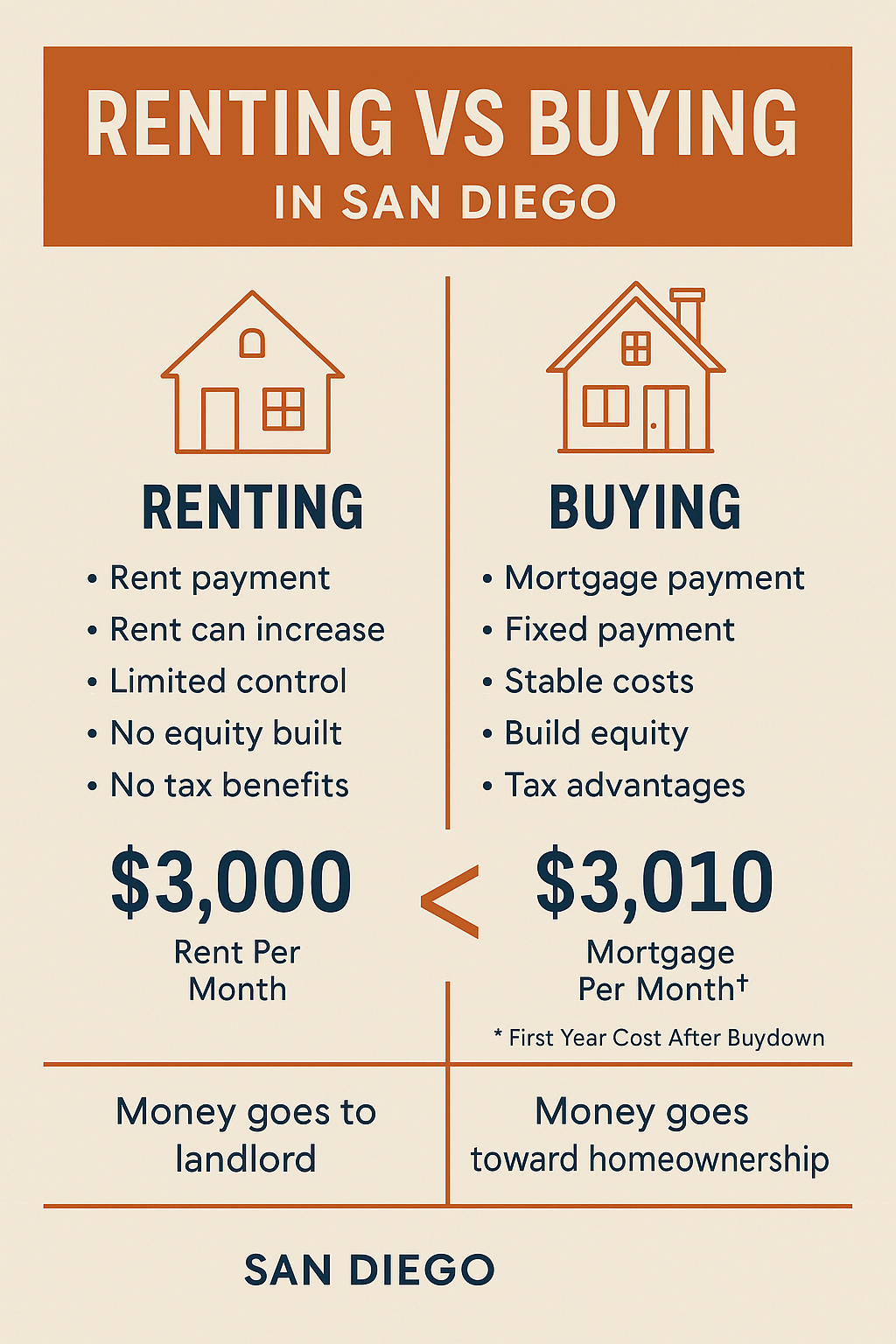

📘 Chapter 7: Real Story — From Renter to Owner in Under 45 Days

A couple in Mission Valley was paying $3,000/month for a 2-bedroom apartment.

They assumed they didn’t qualify to buy.

Turns out they were wrong.

After reviewing their info:

-

They qualified for 3% down

-

Seller paid ALL closing costs

-

We negotiated a 2-1 rate buydown (saving them $478/month the first year)

-

Their new mortgage? $3,020/month

Essentially the same as rent—BUT now they:

✔️ Build equity

✔️ Enjoy tax benefits

✔️ Locked in housing costs

✔️ Own a home that appreciated $38,000 in their first year

Renting never would’ve given them that.

💬 Chapter 8: What You REALLY Need to Get Started

Most first-time buyers overestimate what they need to buy a home.

Here’s what you actually need:

✔️ A pre-approval

(Not scary. It’s free and takes 15–20 minutes.)

✔️ A realistic budget

We’ll walk through this together.

✔️ A strategy

This includes neighborhoods, loan programs, and affordability options.

✔️ The right agent

Someone who knows:

-

PCS timelines

-

VA loan rules

-

First-time buyer programs

-

San Diego sub-markets

-

Negotiation strategies

-

How to win competitive offers

That’s exactly what I help clients with every day.

🏁 Chapter 9: The Bottom Line — Buying Is the Fastest Path to Wealth in San Diego

You don’t have to buy the perfect home to start building wealth.

You just need to buy your first one.

San Diego rewards homeowners more than almost any city in the nation.

That $430,000 homeowner net worth?

It starts with one step: talking to a professional who knows how to get you there.

👉 Ready to stop renting and start building wealth?

I’d love to guide you through your options.

📞 Schedule a free 15-minute consultation

📩 Request a personalized home affordability plan

📄 Download my free First-Time Buyer Starter Guide

🎖️ Military? Ask me about maximizing your VA loan benefits.

No pressure. No commitment.

Just clarity — so you can make the best decision for your future.

GET MORE INFORMATION